Sample Paper of Accountancy 2014 for class 11, CBSE. Paper No.1

SAMPLE PAPER 2014

Class : XI

SUBJECT : Accountancy

PART A

Q1. Explain ::

(1) Intangible assets (2) Accrual concepts (3) Capital expenditure (4) Matching concepts {3*4}

Q2. The assets of Prakash was P.s 50000 and his liabilities are P.s 10000 at the time of commencement of the business during the year he introduced additional capital of Prakash Rs. 5000 he paid off Rs. 6000 for his liabilities he also withdraw P.s 100 every week for his personnel use compute the profit earned or loss incurred by him during the year {4}

Q3. Show the accounting equation of the following

JAN10. Ram commenced business with cash 80.000 Building 50000 bank loan 20000

11. Paid rent Rs. 3000 including 1000 as advanced

12. Salary Paid Rs.3000 and outstanding Rs.2000

13. Purchased goods from Sam of 5000 & paid him 1/2 of the amount at 10% cash

- goods destroyed by fire cost Rs 500 selling pries 600

- Accrued interest Rs 500

16. commission received in advance Rs 1000 - Withdrew goods for personal use(cost Rs 800 selling pries Rs 1000)

- Purchased furniture P.s 10000 out of which 2000 is for house hold expenses

- Security deposit received from tenant Rs 5000

20. deposited excess of cash over Rs.5000 in bank. {10}

Q4. (a) Mr. Bush has machinery of Rs.60000 On 1st Apr 2000. On 1st Jan 2002 He further purchased a new machine worth £ 500 from DURO INVENTORS Ltd through broker who charges commission of !0% of the value. On 1st Oct 2003 he sold 1/4th of the original machine at loss of 25%. Prepare machinery A/c. Provision for Depreciation AJc & Asset Disposal A/c. If Depreciation is charted 10 %p.a. on reducing balances. Books are closed on 31st march every year.

Note: – {M= Rs. 60) {4}

(b)Mr. Samuel purchased a truck from Tata auto worth Rs.200000 on 1st April 2000 its estimated life is of 10 years. At end of which it will fetch Rs.20000. On 1st Oct 2001 this truck meat a road accident & insurance co. paid claim of 50% of the WDV. On same date he purchased another truck for Rs.300000.and on 1st Jan 2002 he sold this truck for Rs. 250000 through a broker against his commission @ 5 %on selling price. He bought another truck for Rs.150000 on same date rate of depreciation on 2nd & 3rd are 10% p.a. Prepare truck account till the year ended on 31st march 2003 {10}

Q5. An accountant, while balancing his book found that there was a difference of Rs. 270 in the trial balance to prepare the final accounts he placed the difference to a newly opened Suspense Account, which forward to the next year when the fallowing errors were discovered:

(a) Salary for the month of March was posted twice, Rs. 155.

(b) Interest on investments collected by the bankers, were posted directly in concerned accounts through ‘he passbook, but no entrywas made in the bank column of the cash book Rs. 75.

(c) Goods worth Rs. 700 were distributed as free samples but this fact has not been taken into books

(d) Rent of Rs. 350 received from Ranjit credited both to rent Account and Ranjit Account.

(e) A purchase of a chair from Gopal Furniture Mart for Rs. 65 has been entered in purchases book as Rs.56

(f) Old Mathinery sold to the proprietor Rajeev for Es: 400 was entered in Sales Book as Sale to Sanjeev

(g) Cash Purchases from Suraj Rs. 189 were recorded in Cash Book as well as in Purchases Book and posted from Both.

(h) Closing Stock has been under valued by Es. 300.

(i) Rs. 300 paid to Rajeshwari was posted to the credit of Rajeshwar

(j) Rs. 450 received from Renu & Co. was posted to the debit of their account.

(k) Rs. 200 being Purchases Returns was posted to the debit of Purchases account {10}

Q6.

(a) Mr. Don founds his bank statement showing: debit balance of Rs. 45.000as on 31″ March 2.008. He noticed following discrepancies:

1) Cheque of Rs.20, 000 lodged with bank of which Cheque of Rs.5, 000 credited in April & cheque of Rs.2000 not cleared at all.

2) Cheque of Rs.6.000, Rs4000 & Rs.3000 issued towards end of year of theses cheque ofRs 4000 is not presented.

3) Pass book shows debit of Rs.250 for interest credit of Rs. 45,000 transferred from fixed deposit a/c.

4) Cheque issued for purchase of machinery Rs30000 dishonored on technical grounds

5) Cheque issued & presented for Rs.5, 500 recorded in debits of cashbook.

6) Debit balance of Rs400 on page No: 36 carried on page 37 as credit balance as Rs 4000.

7) Salary paid by cheque Rs.28.000 was entered in cash book as Rs.2800. {8}

(b) Mr. Jerry founds his Bank account showing debit balance of Rs.50000 as on 31 March 2008.on comparison of passbook he notice flowing discrepancies:

1) Our acceptance of Rs. 1 0,000 for 4 months was retired 2 moths before due date under rebate of 6 % was recorded in cashbook ignoring rebate.

2) 2.Bills of Rs.10000 endorsed gets dishonor was not in records

3) Acceptance of Mohan R.s2000 for two moths 6 By Was discounted @ 12% p.a. not appears in cash book.

4) Money transferred from this account to recurring deposit Rs.3000 not found in cashbook

5) Cheque received Rs 24000 omitted to be banked

6) A postdated cheque ofRs.l,OOO not recorded in cashbook

7) A cheque of RS.2500 banked & credited in PB. & gets dishonored was not recorded in cash book. {8}

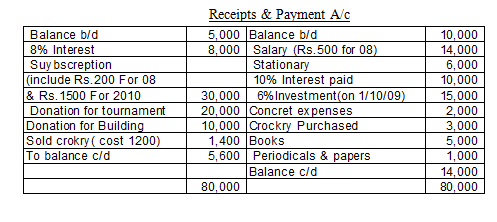

Q7.From the following Receipts & Payment A/c prepare final A/c of CITY CLUB for the year 31/12/09

Additional information

On 1/1/08 The club has building of Rs. 50000; books of Rs. 2000 ; stock of stationary Rs. 1000 & advance subscription Rs. 500 for 2010.

on 31/12/09Salary was payable Rs. 1000 p.m. O/s Subscription Rs. 1500 for 2009 & Subscription still due for 2008 was Rs. 800 {10}

Q22.Opening stock 5,000, sales 16.000 carriage Inward 1,000 sales Return 1,000 profit 6,000, Purchase 10,000 Purchase Returns 900 Calculate closing stock and cost of goods sold. (3)

Q23.X tells you that his capital on 31st December 2008 is 18,700 & his capital 1st Jan. was 19,200 The further informs you that during the year he gave of Rs. 3500 to his brother on private account and withdrew Rs. 300 p.m. for his ersonal

purposes. He also used a flat for his personal purposes, the rent of which at of Rs. 100 p.m. & electricity charges at an average rate of Rs. 10 p.m. were from business account. During the year he sold his 7% Government Bonds 2,000 at 2% premium and brought the money into business. You are required to prepare statement of profit. (5)

Q24.Write short notes on any 2 the following :- (i)Expenses owing. (ii) Unearned Income (iii Contingent Liabilities. ) (4)

Prepared By :

Yogesh Sir ( FOR VICTORY CLASSES)